2026 Market Outlook

- Kevin W. Frisz

- Jan 7

- 4 min read

Updated: Jan 19

January 7, 2026

Legendary football coach Knute Rockne started every new year by reviewing the fundamentals. “This is a football” was his famous first line at the start of a new season. For stock prices, the equivalent of “a football” is “earnings per share”. Corporate profits are the driving force behind stock prices.

“This is earnings per share.”

Earnings per share (EPS) is simply a company’s total profits for a period divided by the number of shares of stock they have outstanding. In other words, if you own 1 share of stock, EPS is your slice of the profits. (Now, you don’t get that amount in a check in the mail. The company and its board decides how it wants to spend those profits. But that’s a conversation for another day.)

Over long-periods of time, earnings per share growth is the overwhelming factor in determining whether stock prices rise or fall.

So, okay. But how does EPS translate into the price of a stock? By the price/earnings multiple (PE). A higher PE means a stock is more expensive, and vice versa.

(Disclaimer: your local MBA student might call bogus on this discussion as being academically over-simplified. And to an extent, they are correct. A PE multiple is a just proxy for a much longer method of valuation. But we are constrained by space, time, and by the fact that most people just use PE anyway.)

Market Valuation

So what is the market PE right now? Below you can see the PE multiple for a basket of 40 large caps in the market today. Ignore the covid era for a second. The market PE drifted upwards from the high-teens in 2015 to the low-twenties today. Currently the market is in the 21-22x PE range.

What’s a key takeaway from this graph? We’re rising, but we’re not “spiking” exactly. A PE multiple of 22x is roughly a 4.5% earnings yield. (ie, EPS dividend by stock price). That compares to the 10yr yield currently at 4.1%.

Company earnings also have the advantage that they are growing most of the time, unlike treasury payments. So, step back a second. Which would you rather have: a 4.1% yield held constant for the next 10 years, or a 4.5% yield that will probably grow over the next 10 years? Hint: you want the second one.

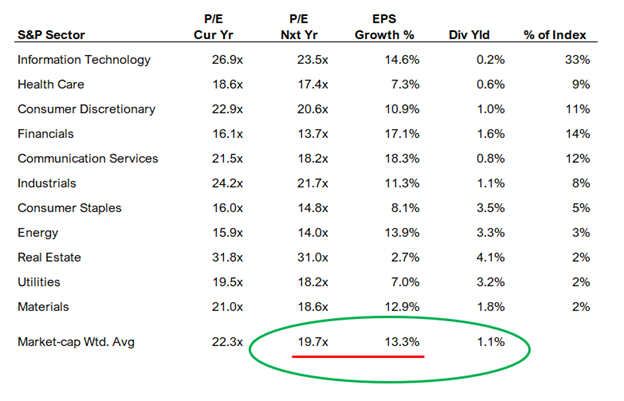

Let’s pull apart the onion a little bit more even. In the table below, you can see the current PE multiples and expected earnings growth by sector.

See that green circle? Those three numbers drive stock prices. That’s it. That’s the whole ballgame. EPS growth + PE multiple + dividend yield. And to be honest, dividend yield is a rounding error in most years. So the two numbers underlined in red are really what we focus on – EPS growth and PE multiple.

So, these two questions will determine the return in the stock market for the year:

(1) How much will EPS grow in 2026?

(2) What will PE be at the end of the year?

Answer those two questions correctly (and often), and you can be a billion-dollar hedge fund manager with a yacht in St. Barts over the holidays!

Earnings Growth

For question #2, we touched on it a bit already. For my worries, I’m focused on question #1. How much will earnings grow. Over the past 3 years, this has been the primary driver of stock market returns – better than expected EPS growth, especially in large cap tech. And most of the earnings growth is concentrated in “info tech” and “communication services” (that sector includes Google and Meta [aka, Facebook]).

So, quite simply: if the market grows EPS at +13.3% this year (as the estimates in the chart suggests), and if the PE stays constant, the market return for this year will be +13.3% plus the 1.1% dividend yield, for a total return of 14.4%.

So, will the market grow EPS at +13.3%? That’s the million-dollar question. For the moment, that growth looks to continue. The secular tailwinds behind more AI spending (and the productivity benefits) still appear to be strong. The Nvidia CEO spoke at the CES conference on Monday and gave very bullish commentary about the demand outlook. Next week, earnings season will start again, and we’ll get detailed comments from all the big companies about their outlooks.

Now, will the PE stay constant? We’re going to review some big-picture risks below. If any of those occur, that PE will fall quickly. (Similar to what happened to the market when tariff talk ramped up last March/April.)

A reasonable BASE case is for earnings to grow 10-15% and for the PE multiple to stay within its current range. That would get us another year of low double digit market growth. What would change my opinion of this? A recession is risk #1. Stocks get crushed during recessions. They just do. Earnings fall, and the multiples fall. It’s all bad. But there also could be surprises to the upside. We might see the emergence of some new AI winner (similar to Nvidia or Broadcom), that would drive upside to the market PE. Think about outcomes in a “range”, rather than in a specific point.

Important Disclosure:

This communication is provided for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any security or investment product. The views and opinions expressed herein are those of the author as of the date of publication and are subject to change without notice. Information has been obtained from sources believed to be reliable, but its accuracy or completeness is not guaranteed.

This material should not be construed as investment advice, tax advice, legal advice, or a recommendation regarding any specific product or strategy. Past performance is not indicative of future results. Any forward-looking statements or projections are based on assumptions that may not come to pass and are subject to change.

This communication is intended solely for clients of Gramercy Private Wealth, LLC and is not intended for redistribution or use by any other persons. Investing involves risk, including the potential loss of principal. Please consult your financial advisor before making any investment decisions.

Gramercy Private Wealth, LLC is a registered investment adviser. Registration does not imply a certain level of skill or training.

Comments